Former Obama fundraiser speaks out against allowing foreign countries to 'pillage' the marketplace.

Don Peebles joins CNBC ‘Power Lunch’ to address the impact of the rate cut on real estate.

Click here to view the full interview.

By Laura Wyatt | Don Peebles

The annual Haute Living's Haute 100 list for 2024 is officially here, celebrating the most influential names in Miami, including philanthropists, entrepreneurs, power couples, developers, creatives, athletes, hospitality power players, and more.

See the full list on HauteLiving.com.

By Laura Wyatt | Don Peebles

Panelists Kevin Hassett and Don Peebles join ‘Maria Bartiromo’s Wall Street’ with their take on former President Trump and Vice President Kamala Harris’ economic agendas.

Click here to see the full interview.

By Laura Wyatt | Don Peebles

The Peebles Corporation founder, Chairman and CEO Don Peebles assesses homeownership in the U.S., housing in NYC and rental costs.

See the full interview on Fox News.

By Laura Wyatt | Don Peebles

Former Obama fundraiser Don Peebles joins ‘Fox & Friends’ to discuss Vice President Kamala Harris vowing to create an ‘opportunity economy’ despite the Biden administration's failing inflation record.

Click here to watch the full interview on Fox & Friends.

By Laura Wyatt | Don Peebles

Mid-century ‘urban renewal’ tore Boston apart. Air rights projects are starting to sew it back together again.

The first construction built over the Mass. Pike since Copley Place is opening now. And more are underway.

Read the full article in The Boston Globe.

By Laura Wyatt | Don Peebles

Former Obama fundraiser Don Peebles discusses the handling of President Biden's exit from the 2024 race on 'Your World.'

Click here to watch the full interview on Your World with Neil Cavuto.

By Laura Wyatt | Don Peebles

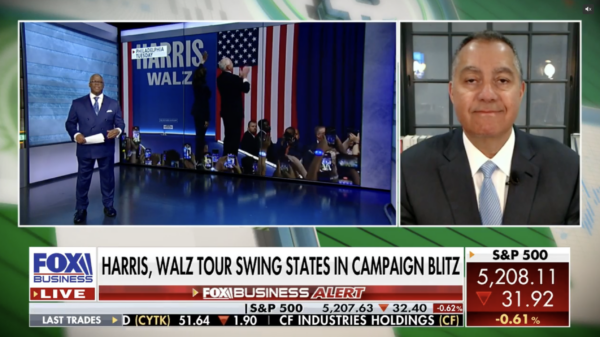

The Peebles Corporation founder Don Peebles discusses the threat of recession and Kamala Harris' economic policies on 'Making Money.'

See the full discussion on Fox Business.

By Laura Wyatt | Don Peebles

Don Peebles, CEO and chairman of the Peebles Corporation, and Libby Cantrill, PIMCO’s head of public policy, join 'The Exchange' to discuss Vice President's potential vice president pick for the upcoming presidential election.

See the full discussion on CNBC Television.

By Laura Wyatt | Don Peebles

THE PEEBLES CORPORATION®

NEW YORK

BOSTON

WASHINGTON, DC

CHARLOTTE

ATLANTA

MIAMI BEACH

SAN FRANCISCO